Diversification is a long-term plan. Basically, the main purpose of a provident fund (EPF) is to allow its members to have retirement reserves after retirement. Investment and retirement planning products in the market include Private Retirement Schemes (PRS) / Unit Trust (UT), etc., which are considered medium to long-term/long-term investment tools.

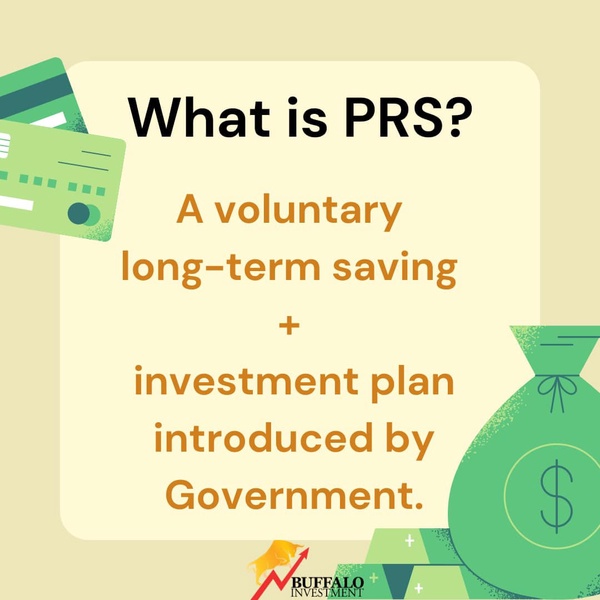

The government has introduced PRS since 2012 to give people more options for planning for their old age. In terms of personal income tax relief items, PRS accounts for RM 3,000 and all risks of the investment must be assessed.

Retirement and education. If you are unable to meet the cost of education, you can also consider education loans/scholarships. But if we don't have enough pension when we retire, there is no such thing as a retirement loan.

In fact, each type of savings/investment tool has its advantages and disadvantages. PRS / UT must rely on good fund managers to minimize risk appropriately. Therefore, choosing a good and qualified advisor manager to invest in it is one of the most important keys. Note: No money games / get-rich-quick schemes!

PRS / UT Investors usually prefer a medium to long-term/long-term / stable and secure investment approach in order to achieve the goals of retirement or children's education/deposit of your 1st house / starting a family / owning your 2nd house / taking a long break from work, etc.

To achieve potentially high returns, you must take on manageable high risks. Asset allocation, the power of medium to long-term/long-term compounding is suitable for people who have no investment experience / less capital and do not want to annoy too much. Therefore, investors need time and patience.

Basically, save enough reserves to cover at least 6 months of living expenses. After that, you can think about the next step and invest your money (available money) such as cash / EPF and so on, make your money work for you and grow it more efficiently (Potential returns 8%-12%). Otherwise, inflation will reduce purchasing power.

Written at the end, there are no shortcuts to investing.

Here are 3 of the most basic rules of thumb:

1) Medium to long-term / Long-term investment (5 years and above) - Think about long-term planning like the rich.

2) Invest regularly - Lazy methods (Convenient and liquidity).

3) Focus on your goals.

Sharing is caring. Of course, the decision to invest or not is still in your hands, your choice. Being young is the cost, come on.

Paul Woon SF is a content creator under the Newswav Creator programme, where you get to express yourself, be a citizen journalist, and at the same time monetize your content & reach millions of users on Newswav. Log in to creator.newswav.com and become a Newswav Creator now!

The User Content (as defined on Newswav Terms of Use) above including the views expressed and media (pictures, videos, citations etc) were submitted & posted by the author. Newswav is solely an aggregation platform that hosts the User Content. If you have any questions about the content, copyright or other issues of the work, please contact Newswav.