House ownership remains a major concern for young Malaysians, as highlighted in the first edition of the Youth Aspiration Manifesto Survey. Conducted by Architects of Diversity (AOD) in partnership with Undi18 and UndiNegaraku, the survey gathered insights from 3,089 respondents aged 18-30 nationwide. According to AOD co-founder Jason Wee, nearly two-thirds (59%) of respondents expressed fears that they might never be able to afford a home. Moreover, a significant majority (90%) of participants urged the government to build more affordable housing for those aged 25-30. Additionally, three-quarters (75%) of respondents supported the implementation of a rent ceiling to protect tenants from exorbitant charges. These findings were presented at a press conference on April 7. But are these fears justified? This article seeks to explore that question.

Unsurprisingly, owning a subsale home in Malaysia’s capital city of Kuala Lumpur comes with a hefty price tag. In the first quarter of 2024 (Q1 2024), the average subsale home price in Kuala Lumpur was RM801,557, surpassing the average price of new homes at RM708,462. According to the Q1 2024 Residential Sales Market Report by real estate technology group Juwai IQI, Sarawak, Sabah, and Johor followed as the next three states with the highest subsale home prices. The report's analysis is based on data from more than 70,000 residential sales in both the subsale and new project markets across Malaysia since 2018.

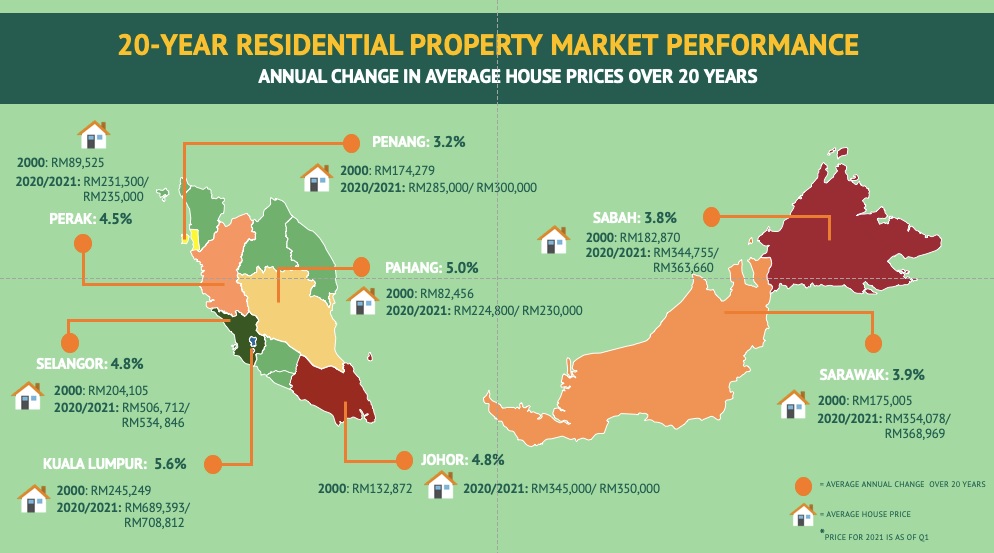

Have houses always been this unaffordable? Let's take a trip down memory lane. In the year 2000, the average house price in Kuala Lumpur was RM245,249. Fast forward to the first quarter of 2021, and that figure skyrocketed to RM708,812—a hefty 5.6% average annual increase over two decades. Now, let’s hop over to Sarawak. In Sarawak, the average house price in 2000 was RM175,005, which climbed to RM368,969 by Q1 2021, with an average annual growth rate of 3.9%. The most dramatic spike happened in 2012, with a whopping 20.52% jump.

Sabah saw a similar trend. The average house price in 2000 was RM182,870, and by Q1 2021, it reached RM363,660, reflecting an average annual increase of 3.8%. Like Sarawak, Sabah's biggest leap also occurred in 2012, with a 13.11% rise. And finally, Johor. Back in 2000, the average house price was RM132,872. By Q1 2021, it had more than doubled to RM350,000, marking an average annual growth of 4.8% over the 20 years. So, yes—houses have indeed become pricier over the years, but the rate of increase varies across the states, with some years standing out as game-changers.

To determine whether young Malaysians, particularly Gen Z, can afford to buy a house, we need to consider some key facts.

1. The Majority of Households Have Limited Emergency Funds

Bank Negara Malaysia reports that 76% of Malaysian households have savings that can cover less than three months of living expenses. This aligns with findings from PIDM, which revealed that most Malaysians have less than RM10,000 in available savings for emergencies. This indicates that many Malaysians may not be well-prepared to handle financial shocks. The situation is even more challenging for those with irregular income, such as your local Grab driver, who often has minimal emergency savings.

2. Young Malaysians have ‘burdensome’ debts

According to the UCSI Poll Research Centre, 73% of young Malaysians have taken out loans, meaning nearly three-quarters of them lack the capital needed for financial commitments. As Dr. Hassanudin bin Mohd Thas Thaker, Head of Research and Postgraduate Studies at UCSI University, explains, it's no surprise that many youngsters are in debt. Without enough savings to start a new chapter in life, they turn to loans. The COVID-19 pandemic has only worsened these financial constraints, and inflation hasn’t made things any easier. Dr. Hassanudin also points out that the mismatch between demand and supply keeps this problem ongoing. Adding to the challenge, Bank Negara Malaysia notes that 65% of potential borrowers already have car or personal loans, which could limit their ability to take on a housing loan.

3. Lack of affordable homes

According to Bank Negara Malaysia, to afford a RM300,000 house, a household would need to bring in RM100,000 a year, or about RM8,333 a month. However, here’s the catch: a whopping 76% of Malaysian households earn less than that. Yet, only 36% of newly launched homes are priced below RM300,000. This means that most Malaysians are caught in a financial squeeze, where their income doesn’t quite match up with the housing market. The result? Finding an affordable home feels more like chasing a dream than a reality.

Based on all these, I am sure you will agree that the fears of young Malaysians not being able to afford a home are indeed justified. With the majority of households earning less than what’s needed to buy even a modestly priced home, the financial hurdles are significant. The combination of limited savings, existing debt burdens, and a shortage of affordable housing creates a challenging environment for potential homeowners. As housing prices continue to rise, and with income levels struggling to keep pace, the dream of owning a home remains elusive for many. This scenario paints a stark picture of the financial reality facing Gen Z in Malaysia today.

Aaron Colt is a content creator under the Newswav Creator programme, where you get to express yourself, be a citizen journalist, and at the same time monetize your content & reach millions of users on Newswav. Log in to creator.newswav.com and become a Newswav Creator now!

The User Content (as defined on Newswav Terms of Use) above including the views expressed and media (pictures, videos, citations etc) were submitted & posted by the author. Newswav is solely an aggregation platform that hosts the User Content. If you have any questions about the content, copyright or other issues of the work, please contact Newswav.