Last week, Reuter has reported that EPF plans to sell its local education assets worth more than RM500 million by winding up of its investment in Alpha REIT. The disposal is reported to be part of EPF annual investment portfolio rebalancing exercise.

Alpha REIT’s assets are all focused on top-tiers international schools in Klang Valley - Sri KDU school, the International School @ ParkCity and Eaton International school. Alpha REIT was incepted in 2017 and has performed with total returns and yields exceeding 6% up to 2021, as reported by The Star dated 13 January 2023.

So, what has happened? Are the plans to rebalance EPF education assets during current market fears are appealing strategy?

The rising interest rates trends globally may have dented the appeal of REITs investment. Arguably, getting attractive valuation to dispose these assets can be a long shot.

Is EPF letting go of its goose that lays the golden eggs?

Recently, a local group has appealed to the Prime Minister for early EFP withdrawal prior to mandated retirement age to meet immediate financial distress such as overdue bank loans and losing jobs.

This is not new. During coronavirus pandemic lock-down, the government has already allowed four rounds of early withdrawal as immediate solution to the contributors’ financial constraints. This is despite being cautioned by local economists, analysts, consumer associations and EPF itself.

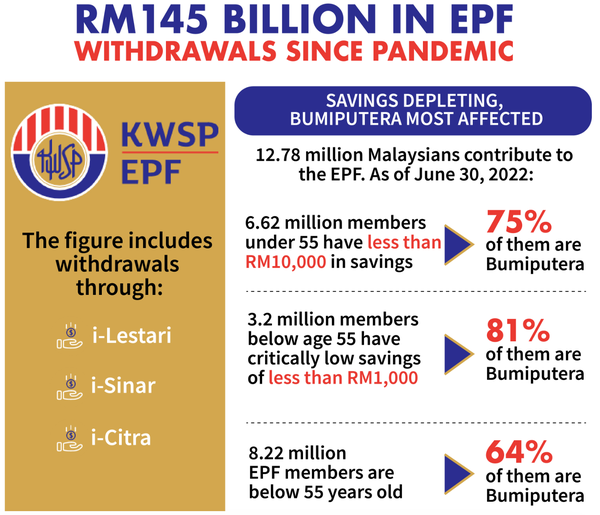

So, what is the “big surprise” when EPF reported that 5.1 million (76%) of bumiputra EPF members below mandated retirement age has savings less than RM10,000 at the end of financial year 2022 (NST). What is more disturbing is that the median for bumiputera members have dropped from RM6,600 in 2021 to RM4,700 in 2022 falling short of minimum target of RM240,000 of basic minimum savings for retirement.

Scheme that allows early pension withdrawals is not only practised in Malaysia. Other countries like Australia and the US have done in a similar way to deal with the pandemic. While there are variations among countries, Malaysia has at least two red flags from the rest.

Firstly, only 3% of EPF contributors are estimated can afford their retirement as quoted by EPF (The Star). Thus, EPF can no longer be their lifeline unless the retirement age is being raised.

Secondly, the EPF has disclosed that the costs of EPF withdrawals for all four rounds of special withdrawal schemes that have allowed by the government (namely i-Lestari, i-Sinar, i-Citra and a special withdrawal programme) was amounting to RM145 billion. (NST)

This is a classic example of policy dilemma. It is quite possible to be sympathetic to the members’ plight so that they can solve their financial problems. At the same time, EPF has a mission, which is to help Malaysian workforce to have enough savings upon their retirement.

As only 3-4% of current Malaysian workforce can afford to retire, the government is arguably not doing any favours by allowing another special withdrawal. In fact, another round of special early pension withdrawal will trigger EPF to sell more of its assets under pressure. Obviously, the return on these investment will be less attractive especially during this volatile market, translating into mediocre annual dividends to the members.

In these challenging times and unfavourable outlook ahead, we need different “medication” to help those who are in financial needs including B40.

Here’s the analogy. If the pain is too “unbearable”, the government may continue to give the “same medication” as before. At the same time, all of us must be prepared that “this short-term medication” has severe “side effect”. There are enough red flags to indicate the risk of retirement crisis and inability of current social security framework to support increasing ageing society. While the impact may not be immediate, the call for “other treatments” is urgent and should be targeted.

Azlan Jaafar is a content creator under the Newswav Creator programme, where you get to express yourself, be a citizen journalist, and at the same time monetize your content & reach millions of users on Newswav. Log in to creator.newswav.com and become a Newswav Creator now!

The User Content (as defined on Newswav Terms of Use) above including the views expressed and media (pictures, videos, citations etc) were submitted & posted by the author. Newswav is solely an aggregation platform that hosts the User Content. If you have any questions about the content, copyright or other issues of the work, please contact Newswav.