-T5N-List-(Twitter)-(1).jpg)

By P Gunasegaram

A coordinated effort between health insurers, hospitals, Bank Negara Malaysia (BNM) and the Ministry of Health (MOH) is needed to lower high and rising medical insurance premiums following rising private hospital charges.

The cost of medical insurance is going up at a rate which is so high that medical care in private hospitals is going to be unaffordable for most people, even for those who took medical insurance many years ago to avoid precisely such a situation.

That’s because both insurers and private hospitals are eagerly and jealously guarding their profitability, the burden falling on the person who took insurance because he can’t pay the cost of medical treatment. Now he won’t be able to afford even the premium.

What insurers are doing is to increase premiums so much at the higher age brackets to force people to drop out of their medical plans and therefore avoid having to make high payouts at the time when the insured needs it the most - in old age.

Preposterous, frequent increases

Let me relate my own experience which is for a moderate plan. I had to pay an increase of 50% in premiums from April this year to RM9,819 per year from RM6,546, this in my 71st year when I could least afford it as I am already in retirement.

The premium increases were sharp even before that. In 2018, I paid just RM5,316 in premium and before that RM3,751. In 2006, I paid only RM1,225, showing a sharp increase in premiums over the years. Some eighteen years later when my income is only a tenth of what I earned before, I am paying eight times in medical insurance premiums.

For most of about 25 years of having this policy, I only made three claims - in 2020 and 2021, totalling perhaps RM80,000. For the rest of the time the insurance company had my money for free.

Now they want to increase it by a further 40-70% next year. That means I will be paying about RM17,000 from a base of RM9,819 assuming the worst! I don’t anticipate paying RM17,000 in medical costs so I may drop out, putting the saved costs into a fund for myself.

From RM6,546 in April last year to RM17,00o, in a space of a year is 2.6 times, or a massive 160% increase. How can anyone put up with this? What is BNM doing about it? Why is it even allowing this?

CEO Mark O’Dell of the Life Insurance Association of Malaysia (Liam), despite all the protests, said recently that the proposed increases of 40-70% in premium for next year will remain and increases will only be gradual after that.

That’s preposterous because only this year most premiums at the higher age brackets went up by as much as 50 to 100%. Add on another 40 to 70% on top of that planned for next year, and the increase amounts to as much as 110% to 240% over two years! Ridiculous.

(Here is how I calculated it: At the lower end, we start with 100. It increases to 150 with a 50% increase. With a further 40%, it rises to 210, an increase of 110%. At the upper end, start with 100. A 100% increase takes it to 200. A further 70% increase makes it 340, an increase of 240% from the start.)

Insurers and private hospitals benefit

The problem is not the frequent announcements - they have done that - it’s the preposterous frequent adjustments. The beneficiaries - the insurance companies and the private hospitals, both keen to safeguard their high profits.

This silly, repeated increase in premium far in excess of medical inflation of 12-13%, already double the world average of 5-6% indicates that somewhere along the way someone’s making a lot of money.

It can only be either one or both of the two - the insurers and the private hospitals. Let's take each in turn starting with insurance companies first.

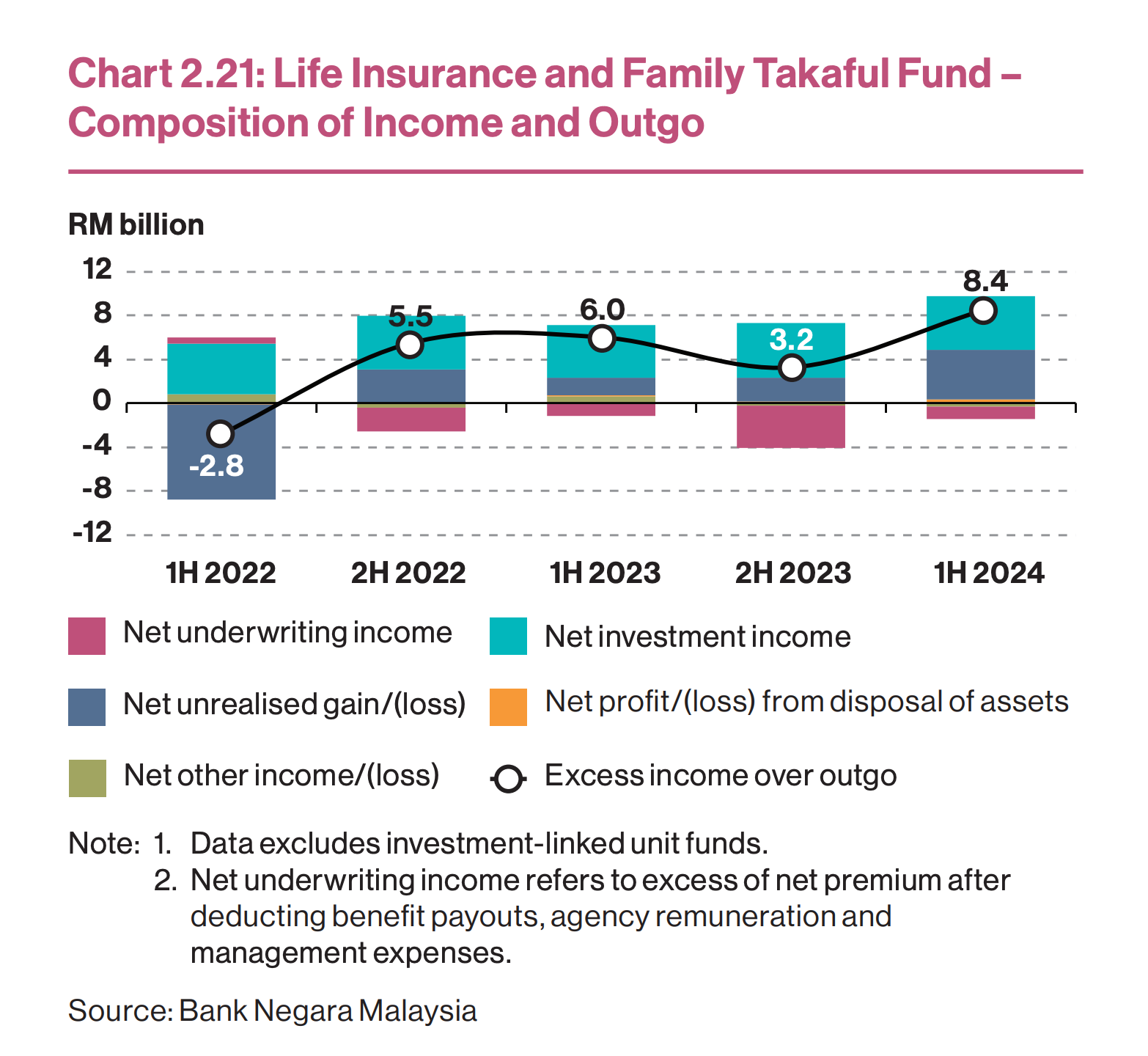

According to BNM’s financial stability report for the insurance and takaful sector, overall profitability of life insurance and family takaful funds was two and half times at RM8 billion in the first half of this year compared to the second half of 2023 when it earnedRM3.2 billion.

That is an incredibly high figure. Bank Negara Malaysia (BNM), the insurance regulator, said that in 2023, Malaysia recorded a medical cost inflation of 12.6%, which is significantly higher than the global average of 5.6%.

If that is so, why is there a need to increase premiums by between 110 and 240% in just two years? How can that be possibly justified when BNM’s latest figures for the insurance industry does not show that it is in any particular difficulty?

Health insurance statistics are hard to come by but one estimate puts it at US$0.92bn or just over RM4 billion in 2024 in terms of gross premium written.

According to another estimate, the Malaysian life insurance industry's gross written premiums reached RM59.7 billion which indicates that medical insurance is just about 6.7% of the total life insurance market.

Insurers in good shape

If the life insurance industry keeps up the same performance in the second half of this year, then full 2024 profit would be around RM16 billion. That represents a huge profit margin of 26.6% on total premiums written, an industry in pretty good shape.

Sure, medical insurance is only a small part of life insurance but with that kind of profit, there is absolutely no urgency to increase life premiums by 40-70% after a massive increase the previous year.

Bank Negara suggested co-payment as a possible solution to the problem of high payouts, but this merely shifts the burden to the insured who shares part of the risk of illness or injury, hardly a solution.

Let’s now move on to the private hospitals, the main culprits and the primary one responsible for all of these problems. Without their ever-increasing, already high costs, this would not have become a major problem.

Private hospitals’ high charges

The most illustrative example of this is Liam CEO O’ Dell’s own experience which he highlighted to the press. He was slapped with a bill of close to RM19,000 for what he described as a minor hernia operation with an overnight stay.

According to O’Dell (above), he did the “simple procedure” at a private hospital in Kuala Lumpur recently, for which he had a one-night hospital stay before being discharged with a 13-page bill totalling RM18,837.55.

“How could a simple procedure with a one-night hospital stay result in a 13-page bill?” he said in an interview with health news portal CodeBlue. How could it indeed, especially for that amount!

There is a huge element of overcharging among private hospitals. Some much more than others. The insured seek the best treatment they can get, and usually they think it’s the most expensive. And the insurance companies pay out but want to maintain their profits.

It's a vicious cycle and the one who comes out the worst for this is the insured who has to pay much higher premiums or drop out altogether, the net result being private health care being consigned to the elite and putting enormous strain on government hospitals to which most will eventually have to turn to.

But this problem can be easily solved. Have a system of standardised charges which ensures both hospitals and insurance companies make money but not too much.

Task force will break vicious cycle

Life insurance companies make tonnes from high-return life insurance policies and therefore they must give some back in terms of medical coverage. Private hospitals must ensure their charges are not totally out of whack with actual costs.

The only way to do this is to set up an independent task force which will make its recommendations and findings public. This will comprise members of BNM, MOH, the insurers, the private hospitals and important and knowledgeable public interest groups. Public input must be encouraged.

There is too little information available now for good decisions. How much does the medical insurance industry make, with breakdowns for each individual one? How much does the life insurance business make, including company breakdowns?

How much does the private hospital industry make? How much do the individual companies within this make? What are all their costs? What are their profit margins? How much are their doctors paid? Etc etc.

Then, with a good task force, who will report their findings and analysis to the public, and indeed seek their feedback before reporting, we will know who is telling the truth and who is lying and by how much. And who is really fleecing who.

That should lead to a rather quick amicable settlement, breaking the vicious cycle of unreasonable and exorbitant rising premiums.

(P Gunasegaram says that good information is absolutely necessary for good decisions.)

P Gunasegaram is a content creator under the Newswav Creator programme, where you get to express yourself, be a citizen journalist, and at the same time monetize your content & reach millions of users on Newswav. Log in to creator.newswav.com and become a Newswav Creator now!

The User Content (as defined on Newswav Terms of Use) above including the views expressed and media (pictures, videos, citations etc) were submitted & posted by the author. Newswav is solely an aggregation platform that hosts the User Content. If you have any questions about the content, copyright or other issues of the work, please contact Newswav.