Your car loan is not your car cost. The real monthly number is almost double that.

Let me tell you about my car situation first, because I think it puts everything that follows into perspective.

I drive a 2013 Perodua Alza. It is fully paid. No more monthly installments. No more ticking off years on a hire-purchase agreement. My entire monthly car expenditure comes to roughly RM130, about RM80 in fuel at ten litres a week, RM50 in tolls and parking combined. My insurance and road tax together cost around RM500 a year, which works out to about RM42 a month. All in, I spend approximately RM172 a month to keep my car on the road.

It took years of loan payments to get here. And it was worth every ringgit.

But here is the thing. Most Malaysians are nowhere near this point. Most are still in the middle of a hire-purchase agreement, looking at their monthly installment and thinking that is what their car costs them. It is not. Not even close.

The Number You Think Is the Number Is Not the Number

Malaysia has one of the highest car ownership rates in the world. Approximately 93 vehicles per 100 people, which puts us ahead of many European nations. We love our cars. We need our cars. Public transport outside of the Klang Valley corridor is genuinely inadequate for most daily commuting needs, and for millions of Malaysians a car is simply not optional.

But the way most of us buy and budget for cars is quietly causing financial damage that compounds over years.

Here is the fundamental problem. When most Malaysians look at a car, they calculate affordability based on the monthly installment. A Perodua Myvi at RM55,300 on a seven-year loan works out to roughly RM650 to RM700 a month. That feels manageable. Sign here.

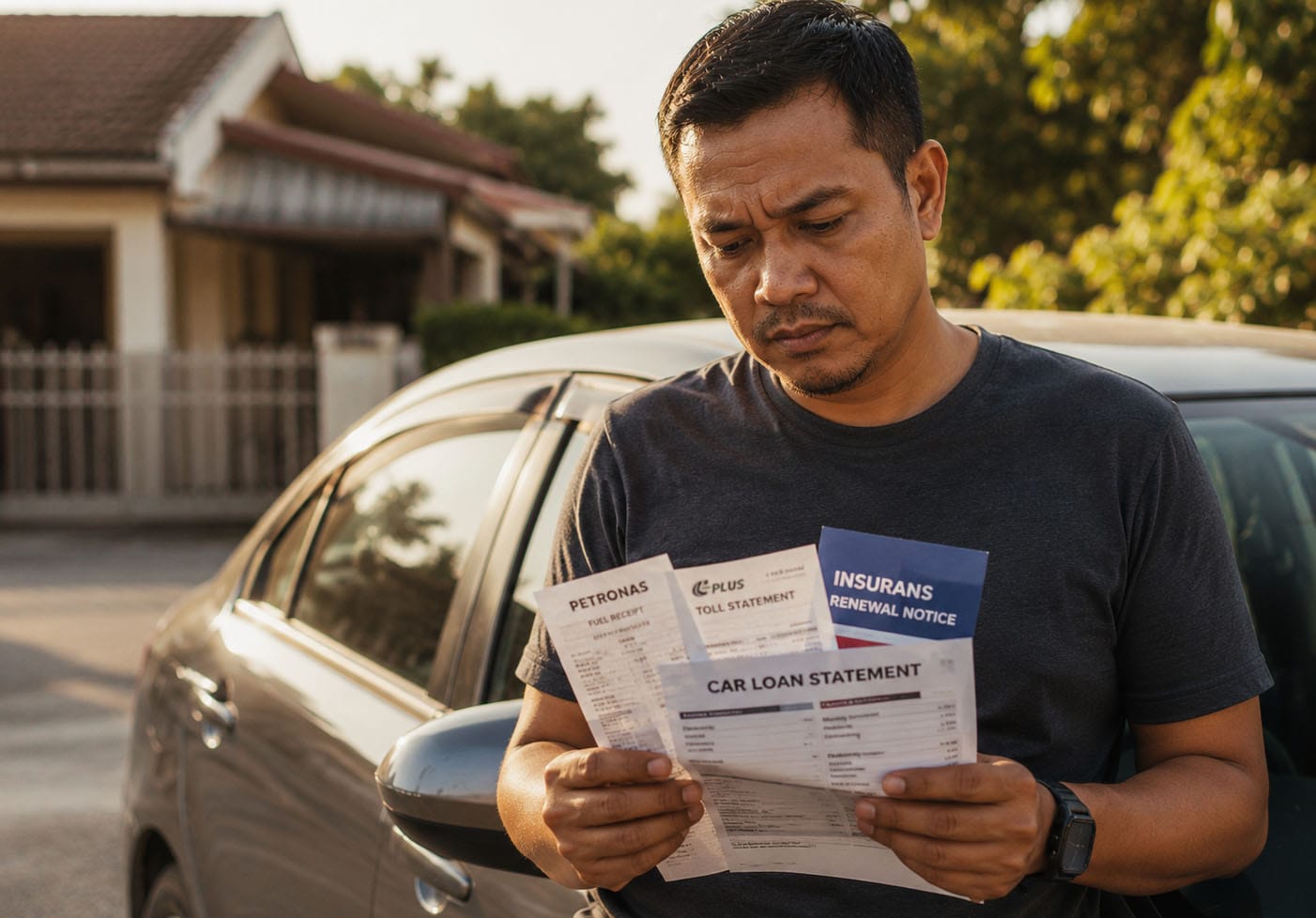

What most buyers do not calculate upfront is that the total monthly cost of owning that same Myvi, once you add fuel, insurance, road tax, parking, tolls, and maintenance, is closer to RM1,100 to RM1,300 a month. Not RM700. Almost double.

For a larger vehicle the gap is even more alarming. A Proton X70 on a nine-year loan carries a monthly installment of approximately RM1,600. But the actual total monthly cost of ownership, including all running expenses, comes to RM2,842. That is nearly double what the showroom brochure implied you were signing up for.

Breaking Down Where the Money Actually Goes

Let us walk through each cost category so this becomes concrete rather than abstract.

The Loan Itself Costs More Than You Think

Malaysian hire-purchase loans for new cars typically carry interest rates of 3% to 3.5% per annum, while used car loans run higher at 3% to 4.5%. These rates are applied on a flat basis, meaning you pay interest on the full principal for the entire loan period regardless of how much you have already paid down.

The practical impact is a nine-year loan costs approximately RM6,480 more in total interest than a five-year loan on the same car. And at the end of those nine years, you will own a car that has depreciated significantly from its original value. A Perodua Myvi bought today for RM55,300 will likely be worth 40% to 50% less in five years. You will have spent years paying interest on an asset that was quietly losing value the entire time.

Insurance: The Cost That Grows as Your Car Ages

Car insurance in Malaysia costs between RM1,000 and RM2,500 per year depending on your car's value, engine size, and your no-claim discount. For a 26-year-old renewing comprehensive insurance on a new 1.5-litre Myvi with a 25% no-claim discount, the annual premium runs to approximately RM1,620. That is RM135 a month just to keep the car legally insured.

The counterintuitive part: as your car gets older and loses value, your insurance premiums should theoretically decrease since the sum insured drops. But if you have ever made a claim and lost your no-claim discount, you know how quickly premiums can spike in the opposite direction.

Road Tax: Small for Small Engines, Painful for Larger Ones

Road tax in Malaysia is calculated based on engine capacity. A typical 1.5-litre engine pays around RM90 per year, which is genuinely negligible. But move to a 2.0-litre engine and road tax starts climbing meaningfully. For larger engines above 2.5 litres, annual road tax can exceed RM1,000. If you are driving a large-engine vehicle, this is a cost that deserves more attention in your annual budget than most people give it.

Fuel: The Cost That Never Goes Away

Compact car owners driving a moderate distance spend roughly RM150 to RM250 per month on fuel. SUV owners and long-distance commuters can easily spend RM300 to RM400 per month. And with the RON95 subsidy review currently underway and global oil supply disruptions creating upward pressure on fuel prices, this cost is unlikely to decrease in the near term.

My own fuel bill of roughly RM80 a month looks very comfortable compared to these numbers. But I also work from home and do not commute daily. For the average Klang Valley worker driving 30 to 40 kilometres each way, five days a week, fuel alone can consume a meaningful chunk of monthly take-home pay.

Toll and Parking: The Hidden Tax on Urban Driving

Daily toll costs for regular highway commuters in Malaysia range from RM100 to RM250 per month. If you are driving from Subang to KL city centre and back daily, your touch-and-go balance is draining faster than you probably realise.

Parking is even more insidious. At RM3 to RM20 per day depending on location, monthly parking costs in urban areas can range from RM150 to RM400. That RM3 per hour at the mall feels harmless in the moment. It does not feel harmless when you add it up across a month.

Maintenance: The Bill That Surprises You Every Six Months

Routine servicing in Malaysia costs between RM200 and RM600 every six months or 10,000 kilometres, depending on your car make and service centre. Budget a minimum of RM100 to RM200 per month as a maintenance allocation and you will not be caught short when the service reminder lights up.

Beyond routine servicing, tyre replacements, brake pads, batteries, and unexpected repairs are inevitable over any car's lifespan. A single tyre replacement for a set of four on a mid-range car can cost RM600 to RM1,200. A battery replacement runs RM200 to RM500. These are not optional. They are just irregular, which makes them easy to forget until they arrive.

The Number That Should Make Every Malaysian Stop

A five-year study of car ownership costs in Malaysia found that the minimum total expenditure over five years of ownership is approximately RM99,512. For a car that may have cost you RM70,000 to purchase.

And Malaysia takes this further than almost any other country. Excise duties of up to 105% are imposed on vehicles, making Malaysian car prices among the most expensive relative to income in the world. We are not just paying a lot to run our cars. We are paying a lot to buy them in the first place, on top of all the running costs that follow.

Over 80,000 Malaysians have been declared bankrupt, with car loans being a significant contributing factor. The monthly installment that seemed manageable on the day of signing becomes a different calculation when life happens, income drops, or the full running cost picture finally reveals itself.

What You Can Actually Do About This

This article is not meant to make you sell your car. In most parts of Malaysia, that is simply not a realistic option. It is meant to help you go in with open eyes.

If you are buying a car, calculate the total monthly cost of ownership before you sign, not just the installment. Add fuel, insurance, road tax, toll, parking, and a maintenance buffer. If that total is more than 20% of your monthly take-home pay, consider a smaller or cheaper vehicle.

Choose the shortest loan tenure your budget can comfortably handle. Every additional year of loan tenure is additional interest paid on a depreciating asset.

If you can get to a fully paid car, protect that position fiercely. The temptation to upgrade to a newer model the moment the loan is cleared is real and persistent. Resist it for as long as your current car is reliable. The financial freedom of no monthly installment is worth more than most people realise until they experience it.

My Take

My fully paid 2013 Alza is not the most glamorous vehicle on the road. It does not turn heads. It has scratches that tell stories I have mostly forgotten. But every month when I calculate my total car expenditure and it comes to under RM200, I am reminded of exactly why I have never been in a hurry to replace it.

A car is a tool. It gets you from one place to another. The best car for your finances is the one that does that job reliably without consuming a disproportionate share of your monthly income.

The monthly installment is not the cost of your car. It is just the beginning of it.

Kamarul Azwan (k.azwan@gmail.com) is a content creator under the Newswav Creator programme, where you get to express yourself, be a citizen journalist, and at the same time monetize your content & reach millions of users on Newswav. Log in to creator.newswav.com and become a Newswav Creator now!

The User Content (as defined on Newswav Terms of Use) above including the views expressed and media (pictures, videos, citations etc) were submitted & posted by the author. Newswav is solely an aggregation platform that hosts the User Content. If you have any questions about the content, copyright or other issues of the work, please contact creator@newswav.com.