You may have seen discussions online about the new medical insurance and takaful initiative: the base MHIT plan.

Some say it's too expensive. Others say the coverage is too limited.

So what exactly is the base MHIT plan?

Whether you already have medical insurance, rely on government hospitals, or currently have no coverage at all, it's worth understanding what the plan actually does and what it doesn't.

Let's take a closer look at five common misconceptions about the base MHIT plan.

1. "The base MHIT plan replaces the public healthcare system"

This is not true.

The base MHIT plan is not national health insurance, and it does not replace Malaysia's public healthcare system.

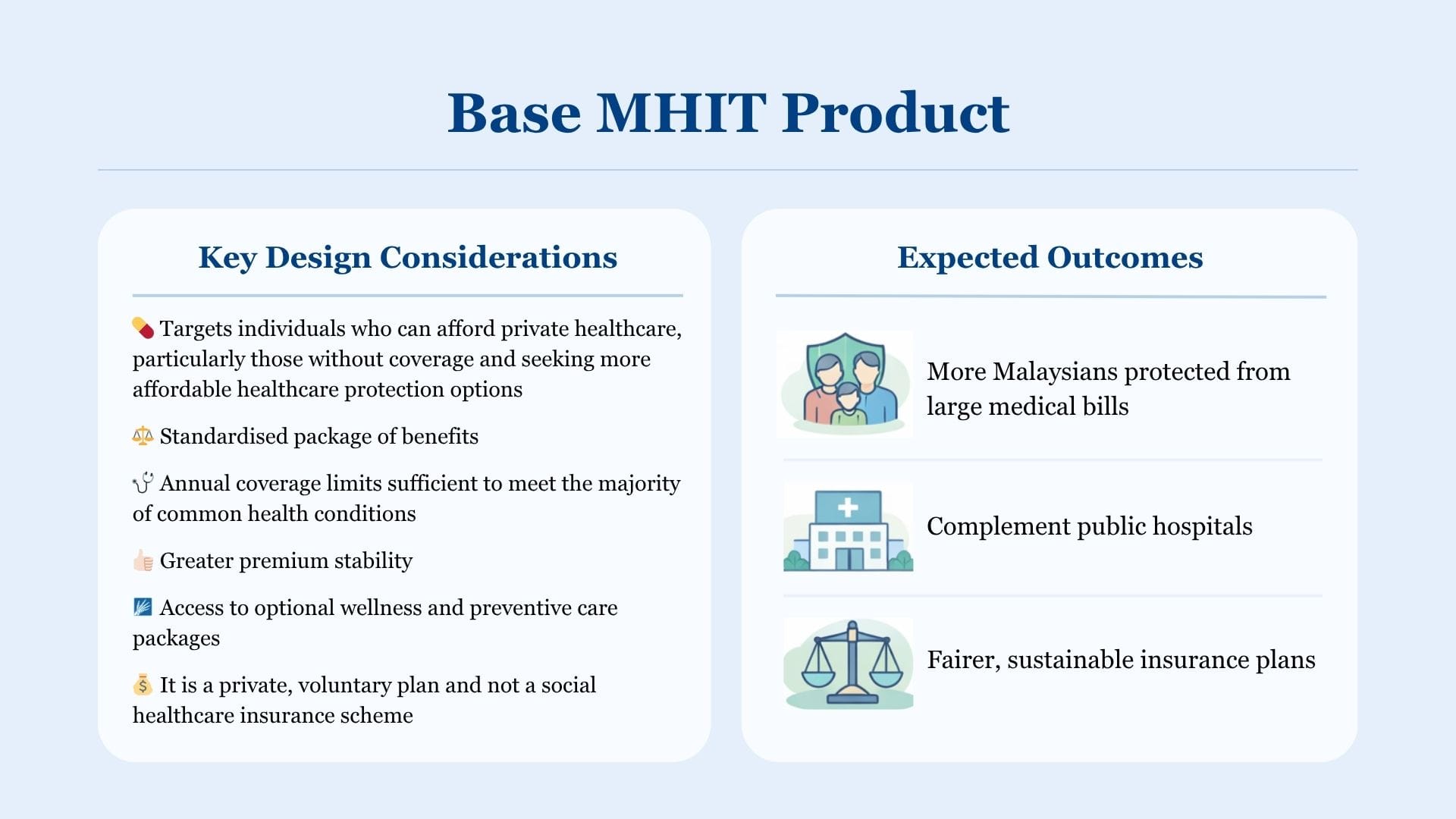

Instead, it is a voluntary insurance and takaful product designed to help address rising medical costs in the private healthcare sector. Like other medical insurance plans, policyholders pay premiums in exchange for coverage that allows them to seek treatment at private hospitals.

What makes the base MHIT plan different is that its benefits are standardised across providers, making coverage easier to understand and more transparent for consumers. It will also be offered as a standalone product, rather than being bundled with investment-linked insurance plans.

Importantly, Malaysia's public healthcare system remains the backbone of the country’s healthcare services. The base MHIT plan simply provides an additional option for those who want faster access to private treatment.

As Associate Professor Dr Muhammad Irwan Ariffin from International Islamic University Malaysia explains: "The base MHIT plan is voluntary and complementary. It does not replace the public healthcare system. Instead, it fills a critical gap between public healthcare and high-end private coverage."

In other words, the goal is to give Malaysians more options while easing financial stress when seeking treatment.

2. "RM100,000 annual coverage isn't enough"

Some critics argue that the RM100,000 annual coverage limit may not be sufficient for complex treatments such as major surgery or advanced cancer care.

This concern is understandable, but it often comes from misunderstanding the purpose of the base MHIT plan.

The plan aims to provide basic financial protection for Malaysians who seek treatment in private hospitals.

Think of it like travel options. Premium plans offer more comfort but cost more. Basic plans provide essential coverage at a lower price point.

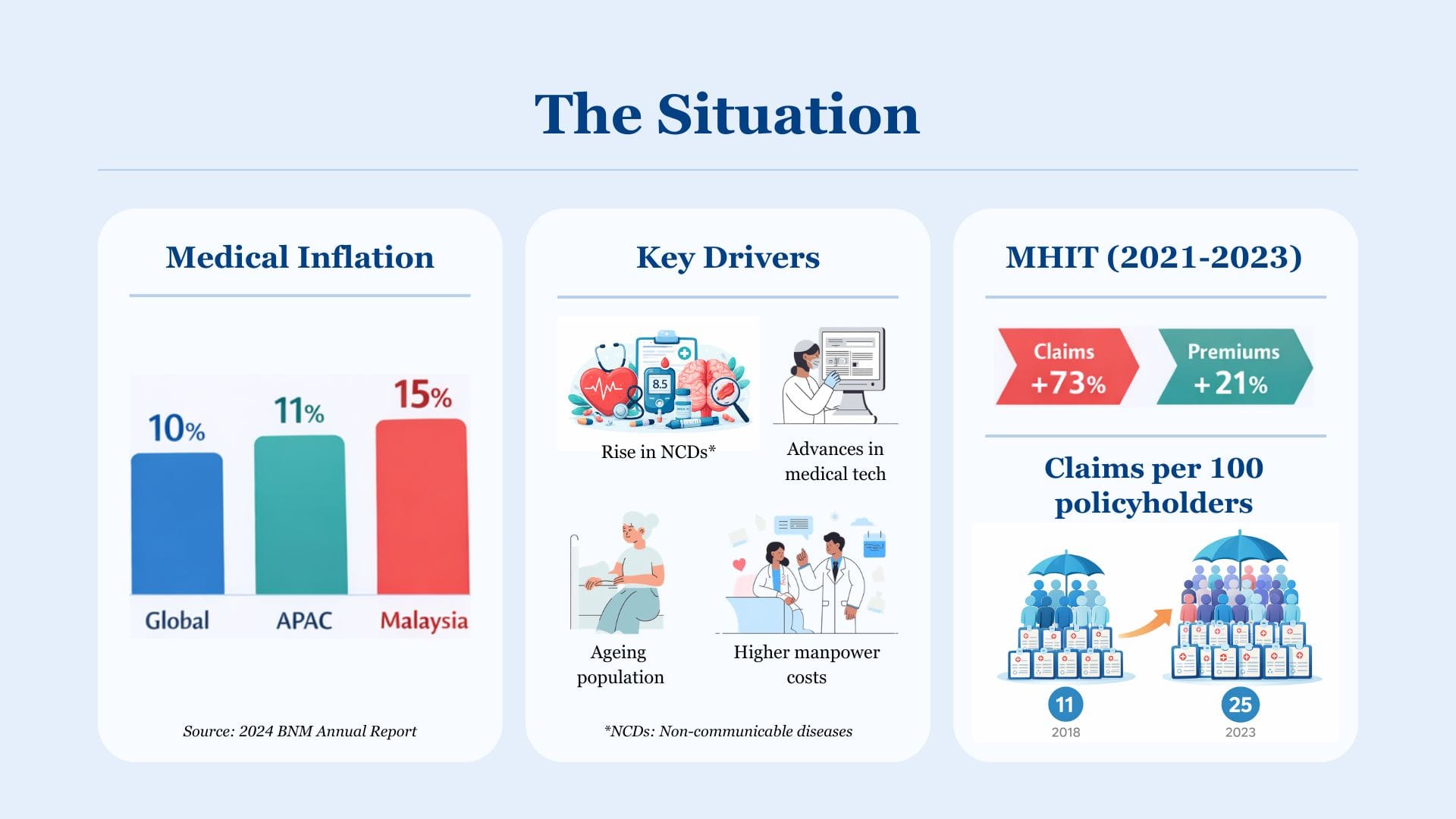

Data from insurers and takaful operators suggests that the RM100,000 annual limit is sufficient for the vast majority of medical cases. In fact, 99% of claims paid in 2024 were RM55,225 or below.

For individuals aged 60 and above, the annual limit increases to RM150,000, and the limits may be reviewed periodically to keep pace with medical advancements.

More importantly, the proposed annual limit is intended to recalibrate current market behaviour, in light of the prevalence of medical plans offering very high annual limits of between RM2 million and RM10 million. While these limits may sound reassuring, they can unintentionally encourage people to use more medical services than necessary, or for providers to offer more treatments than required. Over time, this drives up overall healthcare costs. By setting a more realistic coverage limit, the base MHIT plan encourages more responsible use of healthcare services and helps keep private healthcare affordable in the long run.

In a recent report released by World Bank on ‘Cost Drivers in Malaysia’s MHIT Sector’, it was found that increased utilisation accounts for about 70% of healthcare cost growth, while price increases contribute only around 25%. In other words, medical inflation is largely driven by people using more services or undergoing more expensive treatments per medical episode. This highlights the importance of addressing overutilisation and over-servicing as part of any effort to control rising healthcare costs.

Buying insurance does not mean it should be used unnecessarily. Insurance is meant to protect against significant medical costs when care is truly needed. Overuse of services drives up medical costs and premiums, making healthcare less affordable for everyone. Managing overutilisation helps keep insurance sustainable and accessible.

Consumer behaviour also affects how the market functions. Recent cases of mis-selling highlight this issue, especially where insurance agents aggressively promoted “last-chance” plans with annual limits as high as RM5 million before these products were withdrawn. Such tactics create unnecessary pressure on consumers, pushing them to make quick decisions out of fear of missing out, rather than choosing coverage that truly matches their healthcare needs.

For very complex and costly treatments, the public healthcare system remains available. Those who want higher coverage limits can still purchase additional insurance plans or riders from insurers.

3. "Other plans are cheaper and offer higher limits"

At first glance, some insurance plans may appear cheaper while offering higher coverage limits. However, these comparisons can be misleading.

Insurance products differ significantly in terms of benefits, exclusions, underwriting requirements, and renewal conditions. Some lower-cost plans achieve their pricing by excluding certain conditions, limiting renewals, or imposing stricter eligibility requirements.

Because the insurance market offers such a wide range of products, it is difficult to make direct comparisons between the base MHIT plan and existing plans.

One key feature of the base MHIT plan is premium stability over time. Standardised benefits and broader risk-sharing among insurers help reduce the likelihood of steep premium increases later on.

For Malaysians who want more comprehensive protection, insurers will still offer higher-tier plans and optional riders.

4. "The plan covers all pre-existing illnesses immediately"

Another common misunderstanding is that the base MHIT plan will automatically cover all pre-existing conditions from the start.

That is not the case.

The base MHIT plan is not meant to be a social insurance scheme that provides universal or unconditional coverage.

The plan aims to improve access to insurance for individuals with stable and controlled pre-existing conditions, while still ensuring the long-term sustainability of the insurance pool.

This will be supported by clear and standardised underwriting practices, including waiting periods for certain conditions and clearer definitions of coverage.

One proposal being considered is a "no look back" rule. This would mean that after maintaining continuous coverage for a number of years (for example, 8 years), insurers cannot deny claims due to conditions that existed before the policy started.

Such measures are intended to provide greater certainty and fairness for policyholders, while keeping the system financially sustainable.

These features are still being refined with the insurance industry and medical experts, but the direction is clear, to ensure access, fairness and long-term affordability for everyone who buys the plan.

5. "The plan forces Malaysians to use EPF savings"

Some critics have raised concerns that the base MHIT plan will force Malaysians to use their EPF savings to pay for healthcare.

This is not accurate.

Like many insurance products, the base MHIT plan will offer different payment options. One possible option is allowing members to pay premiums using their EPF Account Sejahtera, which is designed to support pre-retirement needs such as housing, education and health.

EPF already offers a similar programme called iLindung, which allows members to purchase insurance and takaful products.

EPF CEO Ahmad Zulqarnain Onn has explained that having adequate insurance protection helps Malaysians protect their ability to generate income.

In other words, good health coverage supports financial stability — both today and in the future.

Making Informed Healthcare Decisions

Healthcare and insurance decisions can feel complicated, especially when public discussions are filled with conflicting information.

The aim of the base MHIT plan is to create a fairer and more transparent starting point for Malaysians seeking basic medical protection, while helping keep private healthcare accessible.

Several tools under the RESET initiative have also been developed to help Malaysians better understand their options, including:

- FEN's Simple MHIT Guide: A guide to help you navigate your journey to purchase MHIT products and to make claims

- Common Cost Procedures List: A reference to help you understand typical price ranges for 26 common treatments in private hospitals

- Healthcare Budget Calculator: A simple tool to help you estimate how much to save for your future healthcare needs with an MHIT plan

As Malaysia looks for longer-term solutions to rising private healthcare costs, the base MHIT plan is one step towards making coverage easier to understand, more stable, and within reach for more people. It may not answer every concern overnight, but it gives Malaysians something important: a clearer starting point.

And when it comes to healthcare, clarity matters – because better decisions begin with better understanding.