AFTER a strong start in the first quarter of 2026, the outlook for the Philippines' residential condominium property market for the rest of the year is less bright as the Middle East crisis strains remittances, drives inflation, and increases construction costs. One silver lining is the strong performance of the affordable and economic markets in Metro Manila. This was the assessment of real estate advisory firm Colliers Philippines at its virtual Q1 2026 Philippine Property Market Briefing on April 30.

“We are still looking at the impact of the Middle East crisis,” Colliers Philippines Director and Head of Research Joey Roi Bondoc said. “The Philippine property market is cyclical. Periods of economic uncertainty and turbulence usually affect the condominium demand and put downward pressure on prices.”

The Philippines continues to rely heavily on remittances, which reached $36 billion in 2025, while remittances in Q1 2026 totaled $6.5 billion, a figure reflecting 3 percent growth that remains aligned with the Bangko Sentral ng Pilipinas (BSP) forecast, Bondoc said.

A decline in remittances from the Middle East will have adverse effects on the residential market. Lower buyer liquidity will translate to reduced demand, slower take-up, and delayed launches.

Rising inflation will drive already elevated mortgage rates upward to the detriment of the residential market over the next few quarters. “As mortgage rates increase, demand is also dampened,” Bondoc said.

Another possible impact of the Middle East crisis is a decline in condominium completions beyond 2026–2029. He said, “The price of construction materials is increasing, and there will be more adverse impact in terms of take-up for the remainder of the year.”

According to Bondoc, contractors are already operating “under very thin margins," and the continued rise in construction costs may lead to project delays or pauses.

Spiking interest rates and persistently elevated mortgage rates can potentially disrupt the residential property market in the months to come, Bondoc said. Another factor to consider is Colliers’ own forecast of the residential condominium vacancy at an “all-time high” of 25.6 percent, due to the “substantial delivery of new units," particularly in the Bay Area.

To help mitigate these challenges, Bondoc said developers can focus on the following solutions: fast tracking of affordable product pipelines; flexible payment options and promos; leveraging rent-to-own offerings; partnerships with employers and government for housing schemes, and scaling down luxury launches.

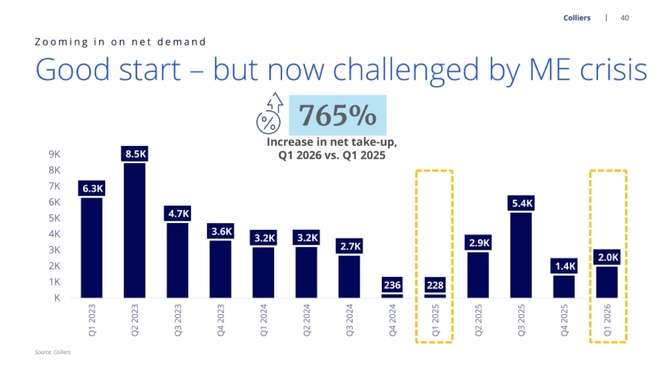

This cautious position for the coming months is a contrast to the residential market’s actual performance in the first quarter. Colliers recorded a 765 percent increase in net take-up in Q1 2026, compared with the same period last year.

Heavy lifting

Colliers' data also showed a shift in demand from luxury and mid-income segments (P3.6 million to P20 million above) to affordable segments (1.8 million to 3.59 million) — which took 74 percent share of recorded net take-ups, an increase of 27 percent from the last quarter.

Bondoc attributed the shift to developers offering attractive payment terms, lease-to-own options, extended down payment terms, and low reservation fees. “It is the affordable and economic segments that are doing the heavy lifting," he said.

Bondoc added that in Metro Manila, both private and public sectors have been implementing reforms and helping drive the demand for lower-priced residential units. He cited the 4PH (Pambansang Pabahay Para sa Pilipino) program as one important driver that is contributing to the strong take-up in the affordable and, especially, economic segments. The government housing program is aimed at addressing the country’s 6.5 million housing backlog by 2028 through the construction of vertical and horizontal housing projects for informal settlers and low-income earners.

“The push for the affordable and economic sector is important because more than 90 percent of unsold units come from this price segment,” Bondoc said. “The government is doing a very good service for the Philippine condominium segment, especially for the urban poor who have yet to own residential units. Hopefully, this represents an organic and more sustainable demand that is contributing to improved inventory life.”

About 2,000 new condominium units were completed during Q1, with the turnover of Shang Robinsons Properties’ Aurelia Residences in Fort Bonifacio; RLC Residences’ Cirrus Residences in the C5 Corridor; and Alveo Land’s Cerca Viento Tower 3 in Alabang. The C5 Corridor accounted for 69 percent of the completed projects.

Close to 13,000 condominium units are due to be completed by year-end, representing a 74 percent year-on-year (YoY) increase, with “a more equal distribution of new supply” across the various Metro Manila submarkets. For this new supply, the Bay Area will account for 32 percent, followed by the C5 Corridor with 26 percent, and Ortigas Center with 24 percent.

Colliers' data showed the lowest inventory life in the past 18 months — pegged at 6.8 years for Q1 2026. Bondoc said, “This is a substantial improvement, much better than the 13.4 years recorded in Q2 2025.”