Half of MARA's borrowers have been blacklisted. Is your name on the list?

The High Court just ordered a woman and her three guarantors to repay RM857,000 in MARA education loans. Meanwhile, MARA's total unpaid debt is closing in on RM900 million. And they are not in the mood to negotiate anymore.

If you have a government education loan sitting in the back of your mind with a "I'll deal with it later" label on it, this article is your wake-up call.

The Numbers Are Not Pretty

Let us start with how big this problem actually is.

Nearly 50% of all active MARA loan borrowers, that is 97,866 out of 197,348 people, have been blacklisted for loan defaults. Half. One in two. The NPL rate at one point hit 49.6%, amounting to RM893 million in non-performing loans. MARA chairman Datuk Dr Asyraf Wajdi Dusuki has made it crystal clear that the days of looking the other way are over.

His message is unambiguous: "We have no right to compromise or forgive deliberate defaulters because every sen disbursed as a loan is public money entrusted to us."

And it is not just MARA. Over 417,000 PTPTN borrowers are currently in default, collectively owing close to RM6 billion. Some of them have been graduated for years, even decades, without making a single payment. When confronted, the most common response is a variation of "I know, I'll settle it soon." Soon has been going on for a very long time.

Why People Default in the First Place

To be fair, not everyone who defaults is doing it out of arrogance or bad faith. The reality for many Malaysian graduates is more complicated than that.

You finish your degree. You enter a job market that pays entry-level salaries well below what you imagined when you signed the loan papers at 19. You have rent to pay, a car loan to service, groceries to buy. Your parents need financial help. Your siblings need support. The PTPTN instalment of RM200 or RM300 a month feels like one bill too many when you are already stretched thin.

So you tell yourself, just this month. I'll catch up next month. And then next month comes with its own set of problems. Before you know it, six months have passed without a payment. Then a year. Then the reminder letters start arriving at your old address and you have conveniently moved.

That cycle is real and it is happening to hundreds of thousands of Malaysians right now.

But here is the thing. The consequences that eventually arrive are far more expensive than the monthly instalments you skipped.

What Actually Happens When You Stop Paying

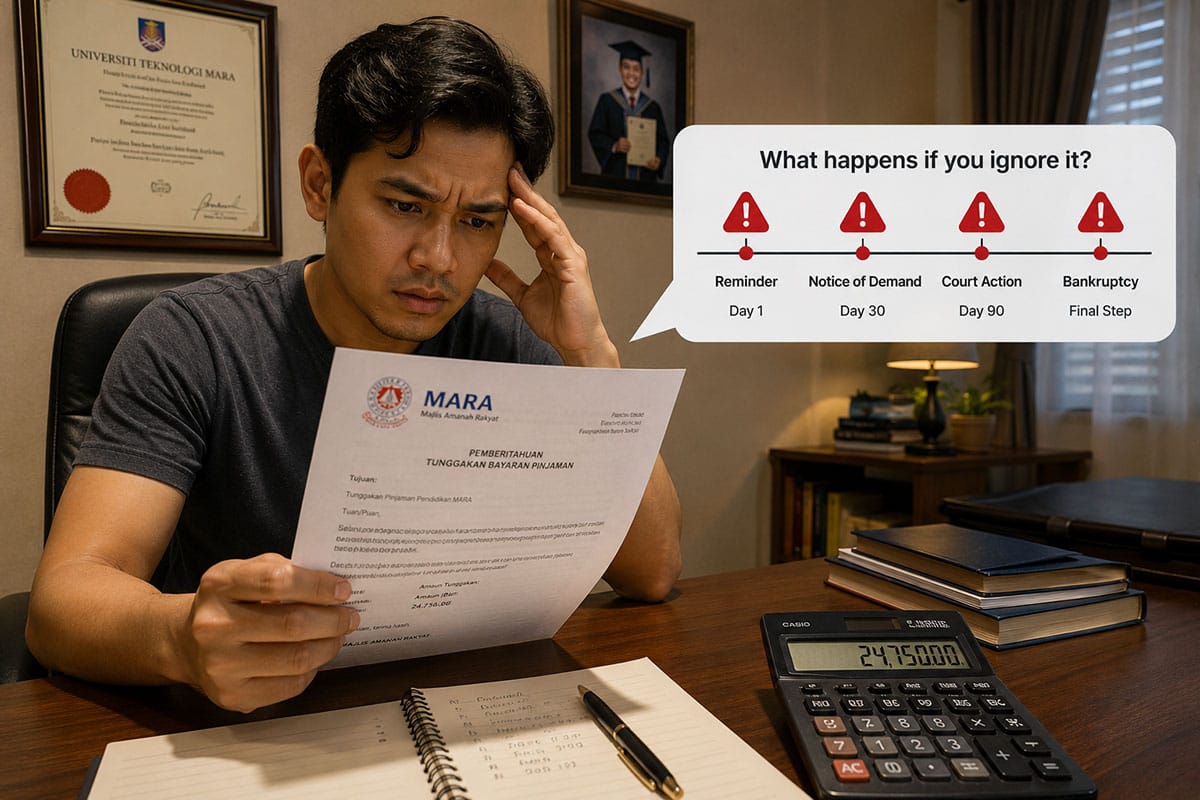

Most Malaysians have no clear picture of the enforcement escalation that kicks in when loan repayments stop. It does not happen overnight, but it does happen, and it gets progressively worse the longer you ignore it.

The process follows a step-by-step escalation. First, reminder letters and SMS notifications. Then a formal Notice of Demand. Then civil lawsuits. If the court rules against you, the judgment can result in wage garnishment, asset seizure, or bankruptcy proceedings. Legal costs get added on top of whatever you originally owed.

For MARA loans specifically, the Cambridge PhD case is instructive. The woman borrowed for a master's degree in Manchester and a PhD at Cambridge. She failed to complete her studies within the agreed timeframe even after an extension was granted. The High Court upheld the full loan agreement and ordered repayment of RM857,000, including her guarantors. Her guarantors, most likely family members, are now legally liable for a debt they did not personally spend.

That last part deserves to sit with you for a moment. By not repaying your loan, you are not just affecting yourself. You are making someone else, someone who trusted you enough to sign their name next to yours, liable for your debt.

For PTPTN, travel restrictions are being enforced in 2026 targeting financially capable defaulters, particularly those earning above RM6,000 monthly or working overseas. Your passport renewal can be blocked. You can be flagged at immigration checkpoints. Additionally, PTPTN reports borrower status to Bank Negara's CCRIS system, meaning missed payments directly damage your credit score and can block future home loans, car loans, and credit card applications.

The Generation After You is Watching

Here is the argument that I personally find most compelling, even as someone who never had a government education loan myself.

MARA and PTPTN exist because the government decided that Malaysians from lower-income backgrounds should have access to higher education regardless of whether their families can afford it. The money that funds your loan today came from tax revenue, from public funds, from the same pool that pays for hospitals, schools, roads, and government services.

When you do not repay, that pool gets smaller. PTPTN has already flagged that sustained default patterns threaten its ability to disburse loans to the next generation of students. Every ringgit that is not recovered is a ringgit that cannot be lent to a Form Five student from Kelantan or Sabah who needs it to get to university next year.

You were helped. You now have the opportunity, and the responsibility, to help the next person. That is how the system is supposed to work.

And for those who are struggling genuinely, this is important: not paying is not your only option. Making a smaller payment than the minimum is still a payment. Showing up with RM50 a month when you can only manage RM50 is infinitely better than showing up with nothing and going silent. MARA and PTPTN have both explicitly said they are open to negotiations for borrowers facing real hardship. The door is open. It is the people who walk away from it entirely that end up in court.

What You Can Do Right Now

If you have a government education loan and you are either currently defaulting, struggling to keep up, or simply not sure of your status, here is what to do.

First, check your current loan status. For PTPTN, log in to myPTPTN app to see your outstanding balance, any arrears, and whether you have been flagged on the travel restriction list. For MARA, contact their hotline at 03-26132000 or visit the MARA official portal directly.

Second, if you are in arrears, do not wait to be contacted. Contact them first. Walk into the nearest branch. Explain your situation. Ask about loan restructuring or rescheduling options which allow you to reduce your monthly instalment or extend your repayment period based on what you can realistically afford. For PTPTN, restructuring can extend repayment up to age 60.

Third, if you genuinely cannot pay the full monthly instalment, pay something. Anything. RM50. RM100. The gesture matters. It signals good faith. It keeps the door open. And it means that when you do face enforcement action, you have a paper trail showing you were trying.

My Take

I did not go to university. Everything I know about marketing, content, business development and digital strategy came from reading, doing, failing, and doing again. So I have no personal stake in the PTPTN or MARA debate as a borrower.

But I have enormous respect for what these institutions were designed to do. The idea that a young Malaysian from a kampung in Kedah or a fishing village in Terengganu could borrow money from the government, go to university, and repay it so the next generation can do the same, that is a genuinely beautiful social contract.

The people who walk away from that contract without paying are not just defaulting on a loan. They are closing a door that someone opened for them, and leaving the person behind them standing on the wrong side of it.

If you borrowed the money, you spent it. You got the education. The degree is yours. The diploma is on your wall.

Now pay for it.

Kamarul Azwan (k.azwan@gmail.com) is a content creator under the Newswav Creator programme, where you get to express yourself, be a citizen journalist, and at the same time monetize your content & reach millions of users on Newswav. Log in to creator.newswav.com and become a Newswav Creator now!

The User Content (as defined on Newswav Terms of Use) above including the views expressed and media (pictures, videos, citations etc) were submitted & posted by the author. Newswav is solely an aggregation platform that hosts the User Content. If you have any questions about the content, copyright or other issues of the work, please contact creator@newswav.com.